Interest Rate Risk

Yield to maturity or internal rate of return on future cash flows is effected by many factors. Duration estimates the change in the price of the bond given a change in interest rates. A second measure convexity improves on the duration estimate by taking into account the fact that the relationship between price and YTM of a fixed rate bond is not linear.

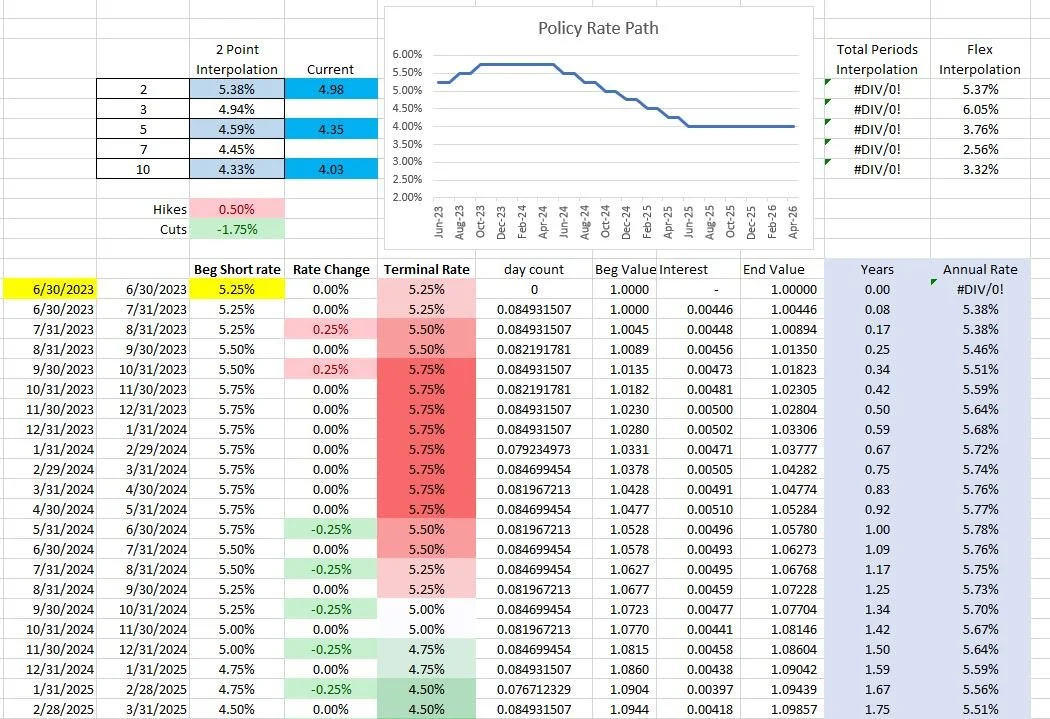

Assuming no default, the bond or portfolio return is impacted by changes in interest rates that affect coupon reinvestment and the price of the bond(s) if it is sold before it matures. That is why having a stead fast understanding of rates is so important to portfolio performance and rate trading. Powell has called for two more rate hikes after this “hike and hold”. So far it looks like the market is set for a pause with some cuts coming in the next 24 months.

The front end of the curve and 2Y note are repriced for an additional 25bps hike.

December SOFR futures are pricing in the long term policy rat to settle in closer to 3.75-4% range.

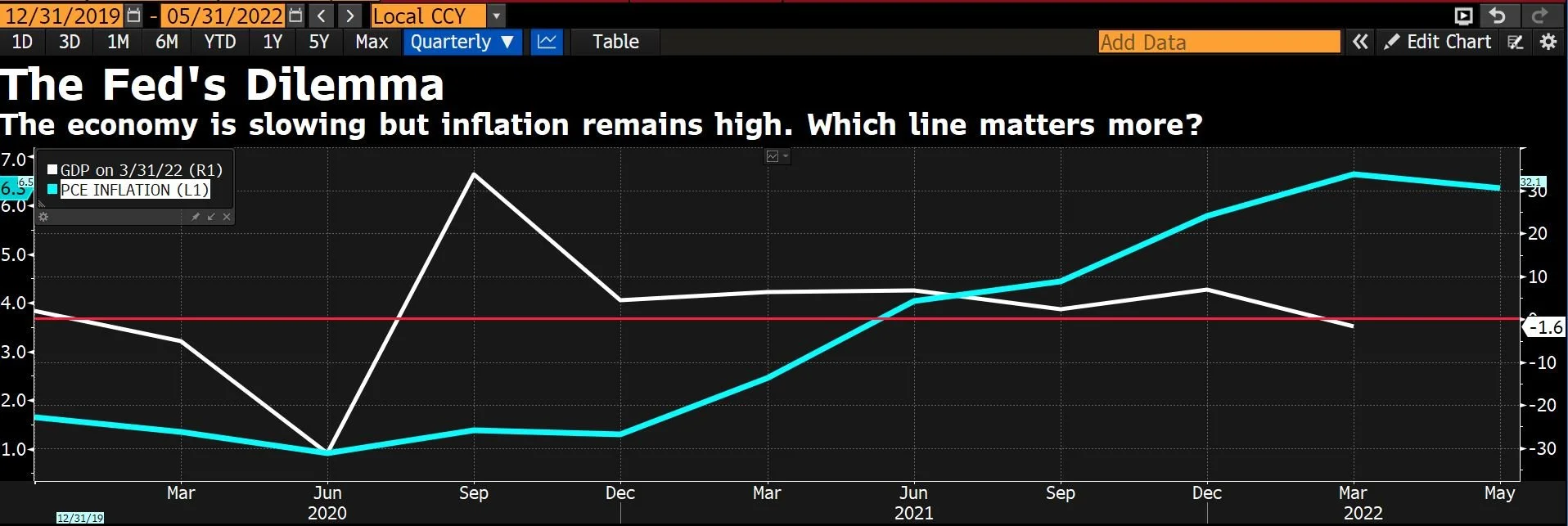

Average hourly earnings remains elevated 4.4% y/y after the latest print. Higher wages and resilience in labor markets is supportive of longer inflation narrative and wage price spiral scenario. . . albeit the bulk of recent jobs have been lower pay jobs in the hospitality sector.

Non-farm payrolls increased 209k in June as average hourly earning and the work week increased a tick. It’s anticipated this will increase headline and core CPI this week.

ISM manufacturing PMI Table is a great resource on the Bloomberg terminal.