Reduced Form Models

Credit rating agencies use ordinal ranking to assign borrowers riskiness from highest to lowest. Ratings do not explicitly depend on the business cycle. Another important point is the issuer pay model for compensating credit rating agencies has the potential conflict of interest in accuracy of credit ratings.

Credit risk analysis has become a staple in the bond portfolio manager toolkit after several credit related financial crisis:

1989 : The “Japanese Bubble” fueled by easy monetary policies and booming real estate/stock markets. Asset prices eventually collapsed, leading to a downturn known as The Lost Decade.

1994-1995: “The Tequila Crisis” and devaluation of the Mexican peso

1997-1998: “Asian Contagion” or Asian crisis that started with the crash of the Thai baht and ended with IMF bailing out South Korea

1998: “ Russian Debt Crisis” a combination of falling oil prices, government fiscal mismanagement, and a highly vulnerable banking sector led to a massive capital flight and a sharp devaluation of the Russian ruble. Russia ultimately defaulted on it’s debt.

2008: “GFC” Global Financial Crisis sowed by the housing market collapse and subprime loans.

Traditional credit ratings were only partially effective in capturing the changes in these correlated default risks. Since then additional measuring sticks to quantify and manage risk have been developed, including estimating correlated default probabilities and recovery rates based on macro-economic factors.

Measures of Credit Risk

Probability of Default (PD): Probability that the bond will default before maturity

Loss Given Default (LGD): Amount of the remaining coupon and principal payments lost in event of default

Recovery Rate: Percentage of position received or recovered in default

Expected Loss: Expected loss = (PD) X (LGD)

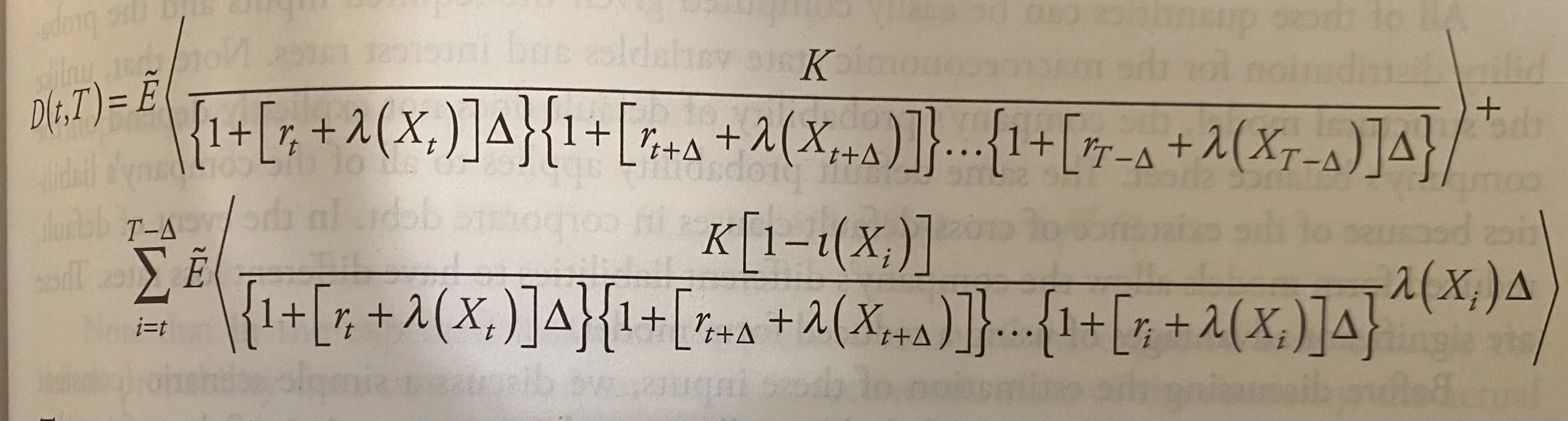

Present Value of the Expected Loss: The largest price one would pay on a bond to an insurer to entirely remove the credit risk of purchasing and holding the bond. The most complex credit risk measure to calculate because it involves two modifications to the expected loss.

Structural models underlie the default probabilities provided by Moody’s KMV. Structural models were used to understand the companies liabilities and to build on insights of option pricing theory. These models are based on the “structure” of the companies balance sheet. However the default probability and recovery rate depend on the assumed balance sheet of the company a weakness in the model.

This is where reduced form models come in handy. Reduced form models for credit risk analysis utilize statistical techniques to estimate the probability of default (PD) for a given entity or portfolio. These models do not explicitly model the underlying factors driving credit risk but instead focus on capturing the overall default likelihood. They incorporate historical default data, market information, and other relevant variables to assess the creditworthiness and assign a probability of default, enabling effective risk management and decision-making in credit portfolios.

Machine Learning and Reduced Form Models

Advancements in Machine Learning combined with traditional credit risk analysis are leading to exciting new models and key insights. Below are some papers I found interesting on the topic.

"Credit Risk Assessment with a Conditional Default Probability Approach" by Jarrow and Turnbull: A seminal paper presenting a framework for estimating default probabilities based on market information and derives a credit spread formula.

"Dynamic Credit Risk Modeling with Intensity-Based Reduced Form Models" by Duffie and Singleton: This paper extends reduced form models by incorporating dynamic features and intensity-based modeling techniques. It introduces the concept of stochastic intensities to capture time-varying default probabilities and provides empirical evidence using bond market data.

"Time Series Models for Credit Default Swap Spreads" by Das and Hanouna: Is focused on time series models applied to credit default swap spreads, a key indicator of credit risk. It discusses the use of autoregressive integrated moving average (ARIMA) models and general autoregressive conditional heteroskedasticity (GARCH) models to estimate credit risk and predict credit spread movements.

Credit Risk Analysis Using Machine and Deep Learning Models: Provides an overview of various machine learning techniques applied to credit risk modeling. It discusses the strengths and limitations of different machine learning algorithms and their relevance in credit risk analysis.